What Many Veterans Don’t Realize About VA Home Loans

A recent survey from NewDay USA found that nearly half of Veterans believe owning a home is out of reach right now.

But for many, that may not actually be the case.

VA home loans have been helping Veterans become homeowners for decades, yet there’s still a lot of confusion around how these loans work and what benefits they offer. In fact, many Veterans misunderstand some of the biggest advantages available to them.

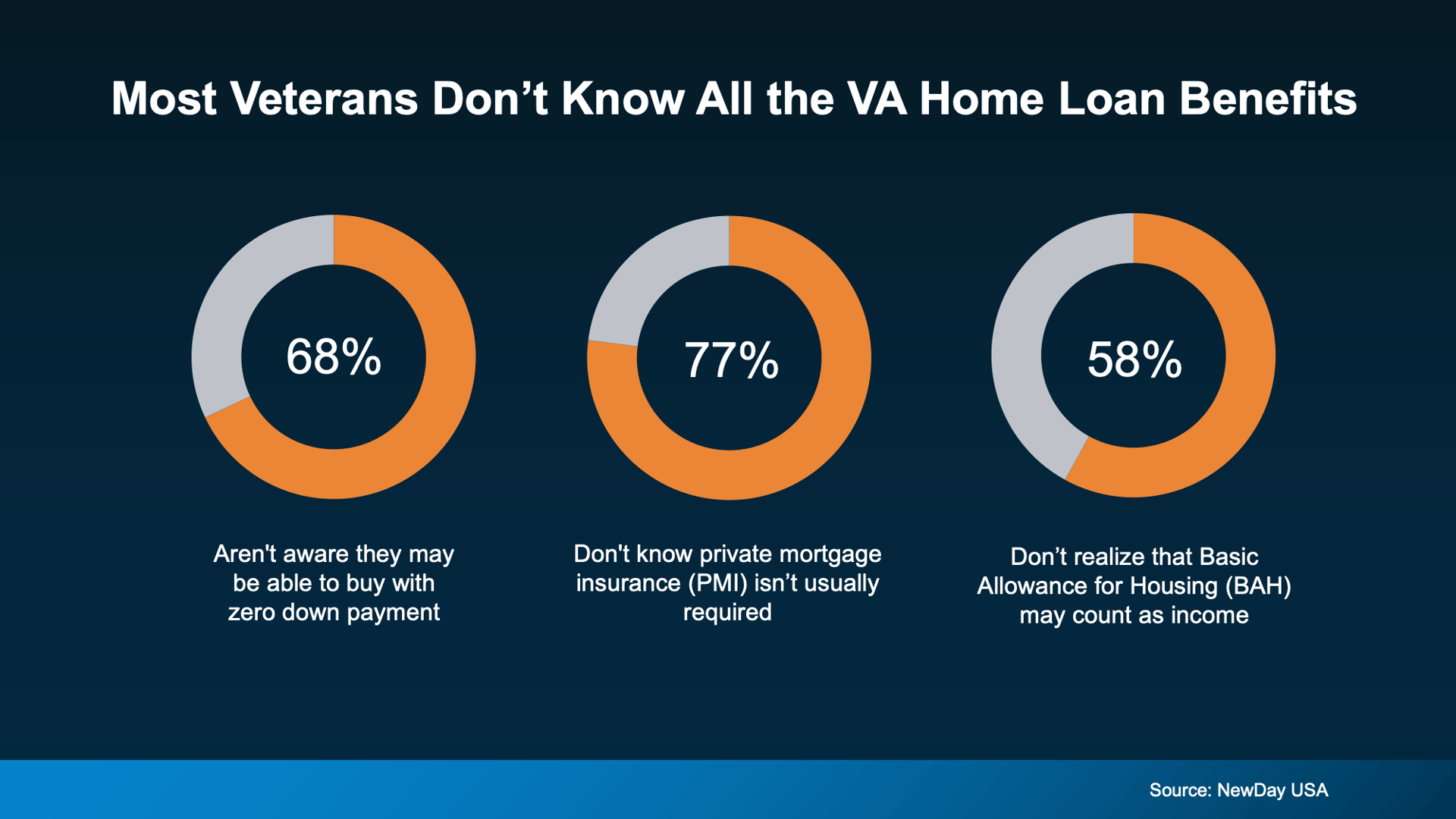

Three misconceptions stood out the most in the survey (see graph below):

If you’ve assumed buying a home requires a huge savings account or expensive monthly costs, it may be worth taking another look at your options.

Some Veterans May Qualify With Little or No Down Payment

One of the most valuable features of a VA loan is the possibility of buying a home without a large down payment.

Many people still believe they need to save tens of thousands of dollars before they can even start the process. According to the survey, a large number of respondents estimated they would need somewhere between $10,000 and $19,900 upfront before purchasing a home.

For eligible buyers using a VA loan, that may not be necessary.

That can make the timeline to homeownership much shorter than many Veterans expect.

Closing Costs May Be More Affordable

Another advantage many buyers overlook is that VA loans can help reduce certain closing costs.

According to the Department of Veterans Affairs, there are limits on some of the fees buyers can be charged when using a VA loan. That can lower the amount of cash needed at closing and make the process more manageable financially.

Combined with low down payment options, this can remove some of the biggest barriers buyers face.

VA Loans Often Don’t Require PMI

Many traditional loan programs require private mortgage insurance (PMI) when a buyer puts down less than 20%.

VA loans are different.

Eligible VA buyers can often avoid PMI entirely, even with a low or zero down payment. That can create significant monthly savings compared to some conventional loan options.

NewDay USA notes that PMI on a conventional loan can cost buyers anywhere from $100 to $300 per month until enough equity is built. Over time, that adds up quickly.

BAH and BAS Could Help Increase Buying Power

For active duty service members and qualifying reservists, Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may also help strengthen loan qualification.

Because these allowances are typically non taxable, they may increase the amount some buyers qualify for when applying for a VA loan.

That means some Veterans and active duty buyers could have more purchasing power than they initially assumed.

Bottom Line

Many Veterans assume homeownership is out of reach before fully exploring what their VA loan benefit can offer.

From little or no down payment options to lower monthly costs and added qualification advantages, VA loans can open doors many buyers didn’t realize were available.

If you’re active duty, a Veteran, or know someone who may qualify, connecting with a trusted lender can help you better understand your options and what steps to take next.